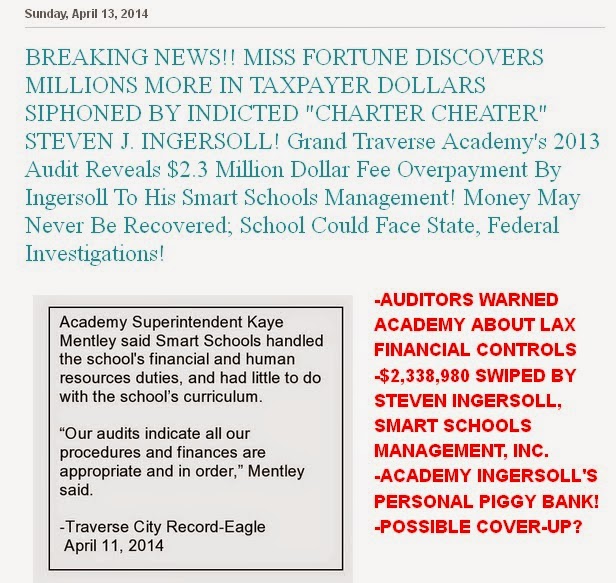

BOARD COVER-UP, EVIDENCE OF INGERSOLL'S "GUILTY MIND"...OR BOTH? In May 2013, Steven Ingersoll asked the Grand Traverse Academy board to help him "avoid adverse tax reporting implications" regarding missing millions!

An order filed today by US District Judge Thomas L. Ludington denying a Grand Traverse Academy motion to quash a trial subpoena issued to the Academy's attorney Meg Hackett may have just broken Steven Ingersoll's federal fraud trial wide open—and dragged the Grand Traverse Academy right in through the gaping hole.

Ludington's order paves the way for Hackett to testify under oath in federal court about a request Steven Ingersoll made during a May 20, 2013 Academy board meeting that the GTA characterize payments made by the GTA to Smart Schools Management, a company owned by Steven Ingersoll, in such a way “to avoid adverse tax reporting implications for SSM and Steven Ingersoll.”

The Grand Traverse Academy, a non-party in Ingersoll's fraud case, filed a motion to quash a trial subpoena in Steven Ingersoll's federal criminal case. The GTA contended that the testimony of Grand Rapids attorney Meg Hackett was privileged and could not be elicited at trial.

The explosive communication at issue concerns so-called “inculpatory statements” allegedly made by Steven Ingersoll on May 20, 2013.” (Inculpatory evidence is evidence that shows, or tends to show, a person's involvement in an act, or evidence that can establish guilt.)

Ingersoll allegedly made these statements to the GTA’s board and attorneys, as well as GTA’s independent auditor and the GTA’s former superintendent, Kaye Mentley.

The GTA motion to quash also sought to quash “the government’s use, reference to or admission of GTA’s privileged communication dated May 30, 2013,” which is a letter from GTA’s law firm (the “Thrun Letter”). Since the filing of the motion, the government has represented that it does not intend to offer the Thrun letter into evidence. Ludington denied the motion to quash the Thrun letter as moot.

GUILTY MIND?

The government originally sought to have the GTA’s attorney, Meg Hackett, testify about Steven Ingersoll’s alleged inculpatory statements. The GTA, however, claimed that Steven Ingersoll’s

statement was “protected pursuant to the attorney-client privilege.”

However, in his order, Ludington determined that the communication at issue—the statements made by Steven Ingersoll during a GTA board meeting—were not protected by the attorney-client privilege.

First, in making the statements, Steven Ingersoll was not seeking legal advice. Instead, the statements requested a “certain characterization of payments so that Steven Ingersoll could avoid serious tax reporting implications.”

Nor were the statements made to Steven Ingersoll’s legal advisor. Steven Ingersoll’s statements were not “made in confidence” because there were several third-parties attending the meeting (either in person or via telephone); the individuals included an independent auditor, an SSM employee, and presumably, GTA board members.

Ludington's order continues, stating “unaddressed by the parties’ papers is the suggestion that the meeting was necessary to resolve questions related to GTA’s audit, a requirement of state law. Thus, Grand Traverse cannot invoke the attorney-client privilege to bar Meg Hackett from testifying about Steven Ingersoll’s statements made at a GTA board meeting.”

THE LEGAL RULING EXPLAINED: MENS REA

Ludington addressed the direct relevancy of Meg Hackett’s testimony is his order.

The bill of particulars in Ingersoll's federal fraud case clarified that the focus of Counts 6 and 7 of the superseding indictment were the payments in 2009 and 2010 from Smart Schools Management and Smart Schools Incorporated to Steven Ingersoll, and not the payments from GTA to SSM & SSI.

Accordingly, the payments from GTA to SSM & SSI were logically irrelevant to those counts. The legal and business relationship between GTA and SSM and SSI remained relevant only to Count 1 and the government’s theory that the defendants engaged in a conspiracy to commit bank fraud in order to assist Steven Ingersoll and SSM to repay the liability to GTA.

Therefore, evidence of the fact of SSM and SSI’s liability to GTA has been admitted.

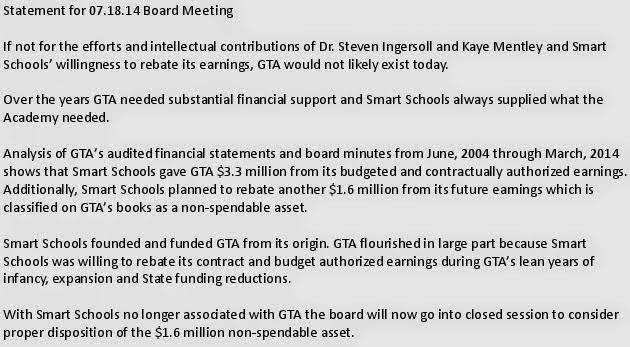

On the other hand, the court had sought to limit introduction of evidence related to competing factual versions of how the liability developed and who was responsible for the liability. (“Thus, GTA’s accounts receivable/prepaid balance has been consistently mischaracterized by the government as an overdraw by SSM when it actually represents SSM’s willingness to support the Academy by rebating budget authorized earnings.”).

However, unknown to Ludington until the Thrun letter was revealed last week was that Steven Ingersoll may have in fact made statements or admissions directly related to his tax liability during the GTA board meeting and thus directly related to Counts 6 and 7.

Ludington concluded that Hacektt's testimony is relevant to Counts 6 and 7 and is also relevant to Steven Ingersoll’s potential motive to engage in the conspiracy pleaded in Count 1.

For centuries, a bedrock principle of criminal law has held that people must know they are doing something wrong before they can be found guilty.

The concept is known as mens rea, Latin for a “guilty mind.”

STILL THINK IT'S A "FOOTNOTE"?

Interviewed by Peter Payette for Interlochen Public Radio recently, Ingersoll defense attorney Jan Geht asserted that the missing millions belonged to Ingersoll. Claiming it was payment made for managing the school, Geht said Ingersoll only owed it to the Academy because he offered to give some of his management fees back when the school was short of money.

Geht called it a “rebate”...and so did the Academy board.